8.83% margin rate (depending on balance)1

75¢ option contracts ($1 for 1st contract)

Stock & ETF trades from $1 (1¢ per share)

Zacks Trade: Built for the Active Trader

Stock & ETF Trades from $1

75¢ Option Contracts

8.83% Margin Rate or Less

Low margin rates

Margin rates start at 8.83% or lower, depending on account balance. Our competitive margin rates offer margin traders big savings compared to rates from other big brokers.1Trading tools for all investors

Trade on a platform that suits your style. Whether you prefer robust tools and charting capabilities or are looking for less-technical way to place trades and manage your account, we have you covered. Plus, trade on the go with the Zacks Trade mobile app.Outstanding support

Our support team of licensed brokers are here to help answer your questions and provide complimentary broker-assisted trades. Connect with a representative anytime from 9 a.m. – 6 p.m. ET, Monday - Friday, by phone or email.Reviews from industry experts

It all sounds great: low margin rates, powerful platforms, actionable research, exceptional customer support… but what do others say? See what 3rd party financial sites are saying.2

Unbiased Reviews from Industry Experts

It all sounds great: low margin rates, powerful platforms, actionable research, exceptional customer support… but is it accurate? See what unbiased, 3rd party financial sites are saying.2

Research to power your trading

Looking for research and market analysis to support your trading decisions? We’ve got you covered. Our clients have access to over 20 free subscriptions to find opportunities and make the most of their trades.

Research to Power Your Trading

Looking for research and market analysis to support your trading decisions? We’ve got you covered. Our clients may utilize more than 20 free subscriptions to find opportunities and make the most of their trades.

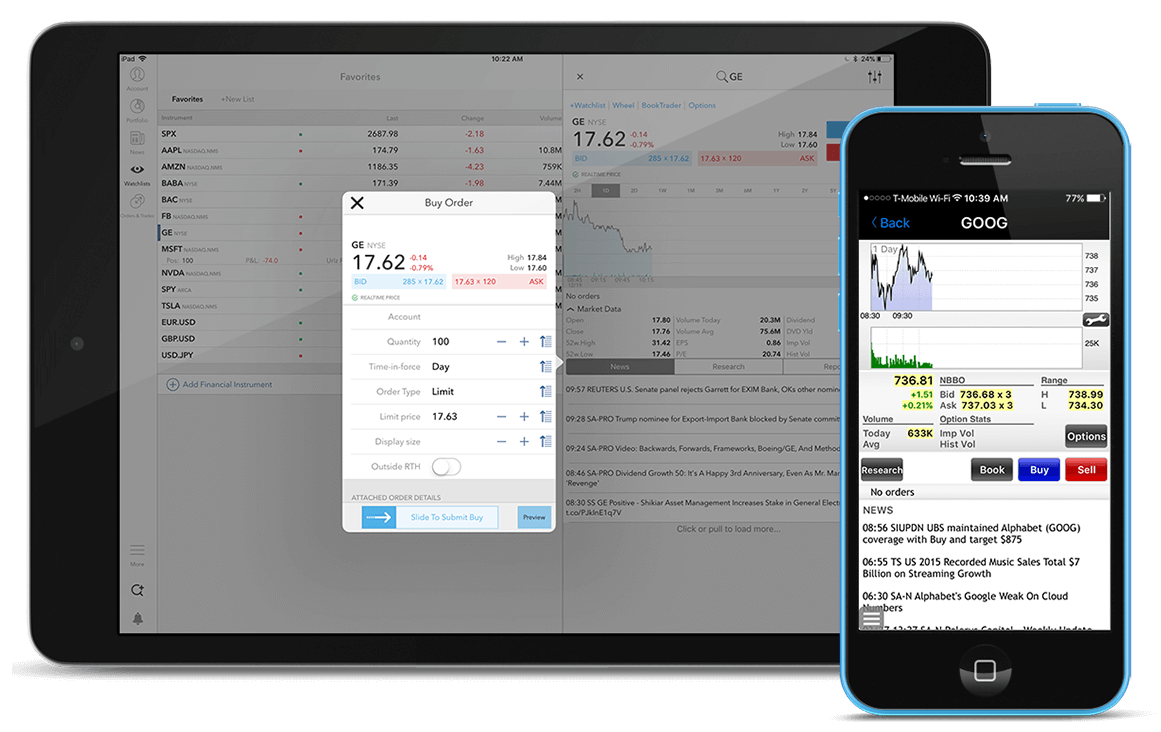

Versatile mobile trading platforms

Want to trade on the go? No problem! The Zacks Trade app works on your smartphone or tablet.

Get to know our options for mobile trading.

Versatile mobile trading platforms

Want to trade on the go? No problem! The Zacks Trade app works on your smartphone or tablet.

Get to know our options for mobile trading.

See why our clients love Zacks Trade2

"Zacks Trade has allowed me to trade and sell more often without being concerned with large fees. Love them! They are always there to help when I need assistance. "

"I can complete trades for less than half of the cost compared to other brokers. They are always responsive and willing to assist and resolve any issues that may arise. They provide all the info I need to make a decision."

"Zacks Trade’s low costs allow me to trade more. Their support staff is very timely in responding and their platforms are user friendly."

"I trade a lot and it adds up. The less I pay in fees the more I have to invest. Their support is always helpful and their platforms are easy to use and understand. "

“Zacks Trade Support is always reachable in a small amount of time. They are courteous and always helpful. I have saved a great deal in margin interest compared to OptionsHouse.”

1Zacks Trade's margin rate starts at 8.83% compared to Charles Schwab (rate starting at 13.575%), E*Trade (rate starting at 14.2%), Fidelity (rate starting at 13.575%), TD Ameritrade (rate starting at 14.75%) and Vanguard (rate starting at 13.75%). Zacks Trade commissions for stocks start at $0.01 per share with a $1.00 minimum. Competitor margin rates obtained from published websites as of 7/27/2023 are believed to be accurate but not guaranteed. Some of the brokers may reduce margin interest rates depending on account activity or margin debit balances. Comparisons do not include competitor discounts or promotions.

2 Testimonials appearing on this site are not considered paid testimonials and are actual client submissions based on individual experiences or clients who have used our products and/or services. However, individual results vary and are not necessarily representative of all those who will use our products and or/services. These testimonials are in no way guarantees for future performance or success. The testimonials displayed are given verbatim except for correction of grammatical or typing errors. Some have been shortened. In other words, not the whole message received by the testimonial writer is displayed, when it seemed lengthy or or the entirety of the testimonial did not seem relevant for the general public. Zacks Trade is not responsible for any of the opinions or comments posted to our site.